How Trump's Tariffs Could Spark a Auto Industry Shake-Up and Boost Your Next Car Cost

President Donald Trump wants to make U.S. manufacturing great again. He might just hobble the American auto industry in the process.

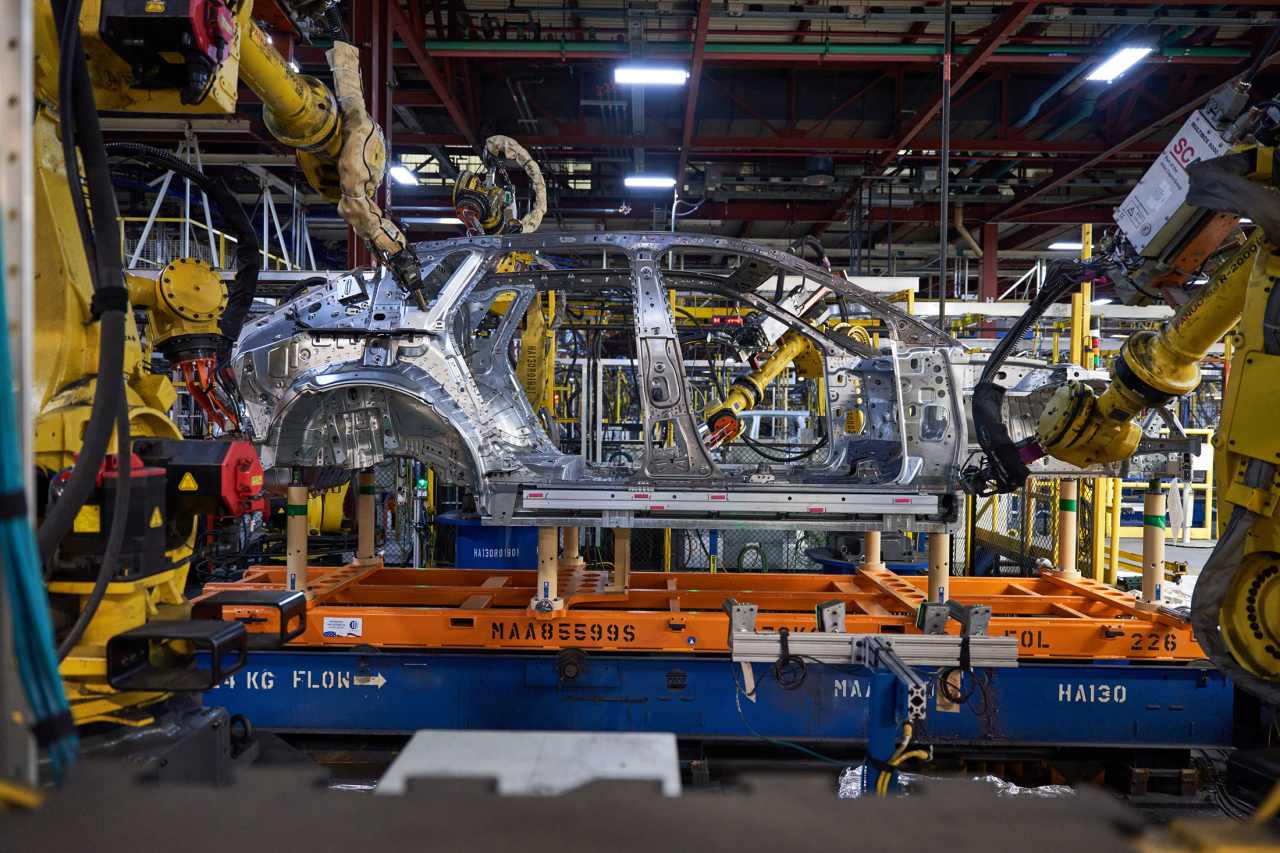

For all the talk of a manufacturing decline in the U.S., auto making remains a huge industry. Half of all cars sold in America are assembled domestically in factories in Michigan, Tennessee, Georgia, and elsewhere, a far larger investment than industries such as clothing or electronics. The current setup uses low-cost foreign manufacturing to produce lower-value parts, while building higher-end components at home.

The U.S. has attracted foreign car manufacturers as well. Toyota Motor, Honda Motor, and Hyundai Motor directly employ some 67,000 manufacturing workers, supporting an additional nearly half-million jobs, while paying an estimated $7 billion in annual wages and benefits at almost two dozen facilities spread across the U.S.

Trump, however, wants an All-American car—parts included—and is willing to use massive tariffs to get one. He has proposed a 25% penalty on imported cars and parts, along with reciprocal tariffs and Section 232 levies on steel and aluminum . After intense lobbying, the president modified the parts tariffs, essentially giving the industry two years to move supply chains back home. He also delayed reciprocal tariffs until July 9, allowing countries time to negotiate.

July 9 is now fast approaching—and the industry remains in wait-and-see mode. The automotive industry could handle 25% tariffs if levies were only on completed vehicles. But similar penalties on car parts will cause far more damage. In 2024, General Motors generated almost $160 billion selling cars in North America, making a profit of $14.5 billion in the process. Tariffs, as proposed, could increase its costs by about $25 billion and wipe out its profits, Barron’s estimates, based on potential penalties applied to import costs.

For now, things aren’t that dire. GM estimates current tariff headwinds of roughly $1.5 billion per quarter, net of cost reductions, or about $2,200 per car sold.

Ultimately, the full load would raise car prices by as much as 15%, Barron’s estimates, based on analyst projections and historical evidence. That would cause U.S. competitiveness to fade and create enough chaos that foreign auto makers could ultimately decide it’s easier to pay the levies than build factories in America. The end result? Car-mageddon. U.S. vehicle sales could plunge by as much as 20%—unless the administration chooses other mechanisms to reach its goals.

“You want to get to a certain local manufacturing outcome, and you’re penalizing yourself by putting tariffs on everything,” says Edward Jones analyst Jeff Windau . “You don’t want to drive the car off the cliff.”

Assembling cars in the U.S. makes sense—and global auto makers know it. In March, Hyundai announced a $9 billion investment to expand production at its Savannah, Ga., plant, the newest car factory in the U.S. It is also building a steel factory to supply its steel stamping plants. The plan to increase U.S. production predates Trump 2.0, but Hyundai CEO Jose Muñoz says localization is the best way to address the tariffs. Still, according to reports, Hyundai is considering raising prices across its U.S. lineup by 1% to offset tariffs, the result of the company’s annual pricing review.

U.S. auto makers are also building more in the U.S. GM recently announced plans to spend $4 billion to retool the Orion Assembly Plant in Michigan, the Fairfax Assembly Plant in Kansas, and Spring Hill Manufacturing in Tennessee, which would add some 300,000 units of production back to America. Stellantis plans to reopen its Belvidere Assembly Plant in Illinois. Ford Motor already assembles more cars domestically than its Detroit peers. All told, domestic production could approach 75% of demand by the end of the decade, based solely on tariffs placed on completed cars.

“We have excess manufacturing capacity at our existing plants, and auto companies can easily bring good union jobs back to the U.S.,” says UAW President Shawn Fain .

That’s not the case if tariffs on car parts are imposed as currently proposed. The auto supply chain is spread across the world to make it as efficient as possible, with cheaper components made in low-cost countries. Ontario-based Magna International, for instance, has more than 340 manufacturing facilities in 28 countries. It makes hundreds of products, including the e-axle—a high-tech drivetrain component that integrates gears, an electric motor, a power inverter, and an axle for the Ford F-150 hybrid pickup truck.

The e-axle is an international piece of machinery. The gears and motors are made by Magna suppliers in the U.S., Canada, and Mexico. The power inverters come from the U.S. The casings come from Mexico. They all get shipped to Canada for subassembly. Then the finished parts are shipped to Ford’s Dearborn Truck Plant outside of Detroit.

“This kind of cross-border coordination is common in our industry,” says Magna’s vice president of operations, Kathy Worthen. “It also shows why stable trade relations and efficient logistics matter so much—not just for [car makers] but for the entire supply chain that builds the modern car.”

The benefit to consumers of lower-cost manufacturing is improved affordability. That will “simply be out the window,” says David Greene , head of industry and marketplace analytics at Cars.com, adding that there will be precious few new cars costing less than $30,000 when the full effect of tariff policies is felt. Prices are already starting to rise. Cars.com counts an average price increase of about $1,100 for Mexican-built vehicles since the start of 2025. Used-car prices increased by 6.5% year over year in June. Buyers can expect the average car price to creep $1,000 to $2,000 higher over the next 12 months.

Ford CEO Jim Farley puts it more succinctly: “We’ve got to make sure the parts are available, even [foreign] parts.”

The president’s One Big, Beautiful Bill Act tries to offset that somewhat. It would eliminate electric-vehicle purchase tax credits worth up to $7,500 and replace them with a deduction for car loan interest for U.S.-assembled vehicles of up to about $1,000. The only problem: To get the full credit requires buying a car that is expensive enough to hit a $10,000 interest cap. Maybe sales of the $160,000 Cadillac Escalade V or a $200,000 Corvette ZR1 will get a boost.

The uncertainty around the final forms of the tariffs is already having an impact. A new factory can take up to five years from breaking ground to producing vehicles. The combination of potential parts tariffs, the on-again/off-again nature of their implementation, and country-by-country trade talks—which industry executives fear could favor one nation over another—have some auto makers opting to retool existing plants or simply manufacture overseas and pay the tariff.

“Many companies are hitting the pause button because they don’t know what the rules are going to be a week, a month, or a year from now,” notes Capital Group economist Darrell Spence.

The longer-term effect on the industry could be devastating. The fact that Trump plans to penalize all parts coming into the country forces new costs on U.S. auto makers that others don’t bear, making U.S.-made cars too expensive for foreign markets, killing GM, Stellantis, and Ford’s ability to export cars. Take steel, which isn’t specific to just autos. The 50% penalty “hurts,” says John Pfeifer, CEO of fire engine maker Oshkosh. “They increase the input costs we all have as [U.S.] manufacturers…. Steel and aluminum are cheaper in Europe and Asia.”

More expensive materials, with a lack of low-cost parts, manufacturing scale, and specialization, could easily raise the cost to make a 100% U.S. vehicle by $10,000, or more, dangerously close to offsetting any penalty from importing whole cars.

A decade from now, the current policy regime, with tariffs on parts and imported vehicles, would make the U.S. car industry landlocked, less profitable, and smaller relative to the global industry. “Tariffs lower long-run productivity by both raising input costs, reducing investment, and distancing U.S. firms from competition,” says Ernie Tedeschi , head of the Budget Lab at Yale University. “By extension, they lower long-run real wages too.”

The tariffs could even accelerate the arrival of Chinese cars in the U.S., argues BofA Securities analyst John Murphy , setting up a dynamic similar to the arrival of cheap Japanese vehicles in the 1970s and 1980s. Back then, U.S. auto makers couldn’t make smaller, fuel-efficient cars as cheaply as the Japanese and reacted by abandoning the lower-end segment of the market, focusing on larger vehicles with fatter per-car profit margins.

It seemed like a sensible strategy, but it didn’t result in long-term success. Toyota still makes cheaper cars—the average cost for a Toyota purchased in the U.S. is about $42,000, some $12,000 cheaper than the average new Ford—but Toyota generates $1,900 more profit per car despite the lower selling price. The extra profit earned by Toyota turns into updated factories with better scale, producing improved models with new features.

If U.S. tariffs prompt U.S. auto makers to move even higher up the cost curve and abandon more of the lower-priced market, Chinese auto makers like EV leader BYD or Volvo owner Geely Automotive Holdings, with less need to maintain profit margins, could decide to build their own factories and fill the gap.

“The idea that you would have a Chinese manufacturer in the United States sourcing parts from the U.S., employing Americans, and abiding by all the rules, that would come in at the low end, is something that I don’t think is off the table,” says Murphy. “It is literally a matter of time.”

There are better ways to accomplish Trump’s goals. Industry leaders and analysts say focus should be on making the U.S. the low-cost place to assemble cars, with tax breaks and credits for investments and exports used as tools to incentivize production. Murphy likes the idea in Sen. Bernie Moreno’s (R., Ohio) Transportation Freedom Act, which provides additional tax breaks for wages because it lowers employment costs.

Others point to export credits as a way to offset some of the costs. The value of U.S. vehicles and auto parts imports in 2024 totaled some $474 billion, but exports amounted to $169 billion. Meanwhile, Ford makes all of the automatic transmissions in Ranger pickup trucks, assembled in five global factories and sold in 180 markets around the world, in the U.S.

“Ford is almost a net exporter,” says Ford’s Farley. “We have to work with the administration and get some kind of credit. We want to manufacture more in the U.S., but it’s not just keeping it here, it’s actually exporting as well.”

The situation is enough to make investors write off the sector as uninvestible—and many have. Just 15% of Wall Street analysts covering Ford rate the stock a Buy or equivalent, while 27% have that rating on Stellantis, and 48% have it on GM. The average Buy-rating ratio for a stock in the S&P 500 index is about 55%.

All three, however, remain very cheap. GM, Ford, and Stellantis have recently been trading for about five, six, and four times estimated operating profits, respectively. Investors looking for a margin of safety could look for a discount of one point to those numbers before buying.

At those levels and based on operating profit estimates for 2025 and 2026, GM stock would be attractive at $45 a share, down 8% from a recent $49. GM has been relatively strong thanks to its consistent profit margins and stock buybacks.

Ford would be attractive at $10, down 7% from a recent $10.80. Ford’s performance, however, will depend mostly on its ability to improve production quality and reduce warranty expenses.

Stellantis, at a recent $9.60, has 15% upside to reach its margin-of-safety level of $11. It had a terrible 2024 and now has a new CEO, Antonio Filosa , overseeing a turnaround effort. His job, along with managing tariffs, is to repair dealer and employee relations while getting inventories under control.

Auto parts makers have been hit by concerns that production rates will drop off materially in the second half of the year as tariff impacts start to bite. Citigroup analyst Mike Ward suspects things will turn out better than that, setting up parts companies for earnings beats and increased guidance.

One of his favorites is Southfield, Mich.-based Lear, which makes seats and electrical components. Shares, which yield 3.4%, trade for about 7.3 times estimated earnings over the coming 12 months, a discount to its historic multiple closer to 10 times. GM is Lear’s largest customer, accounting for about 22% of sales, and the auto maker’s decision to build a new full-size sport-utility vehicle and light-duty pickup truck at its Orion, Mich., assembly plant will help Lear. Ward has a Buy rating and $123 price target on the stock, up 33% from a recent $92.42.

Aptiv and BorgWarner also look attractive, says J.P. Morgan analyst Ryan Brinkman . Borg, which makes powertrain components and will benefit from more EV and hybrids on the road, trades for just seven times earnings, a discount to its historical multiple of about 8.5 times. Brinkman’s price target for Borg stock is $43, up 29% from a recent $33.46, valuing shares for about 9.5 times his estimated 2026 earnings.

Aptiv, which trades at nine times earnings, also looks cheap relative to its history. The company is splitting into two parts . One unit will supply electrical systems to car makers, while the other will make “sensor-to-cloud tech solutions” for multiple industries. The bet is that a business less tied to cars could fetch a better valuation, since industrial companies in the S&P 500 trade for about 22 times estimated earnings, double the multiples for auto parts companies.

Brinkman has an $85 price target on Aptiv, up 25% from recent levels, valuing the stock at about 10.5 times his estimated 2026 earnings.

Ultimately, investors should be looking for ideas that aren’t completely dependent on tariff policy—and waiting for the right price to pounce when tariff fears beat up the sector.

Write to Al Root at allen.root@dowjones.com

{kind=link}

Post a Comment for "How Trump's Tariffs Could Spark a Auto Industry Shake-Up and Boost Your Next Car Cost"

Post a Comment